3 Reasons Why You Can't Win Despite Backtesting | Fatal Flaws in Manual Verification

"I backtest properly, so why can't I win in the real market?"

Many traders spend dozens or hundreds of hours using the replay functions of MT5 or TradingView, yet fail to see results in live trading. This is a common story.

The truth is, in most cases, the problem isn't the strategy—it's the 'Design of the Backtest' itself.

In this article, we will focus on the three most common fatal design flaws in manual (replay) backtesting.

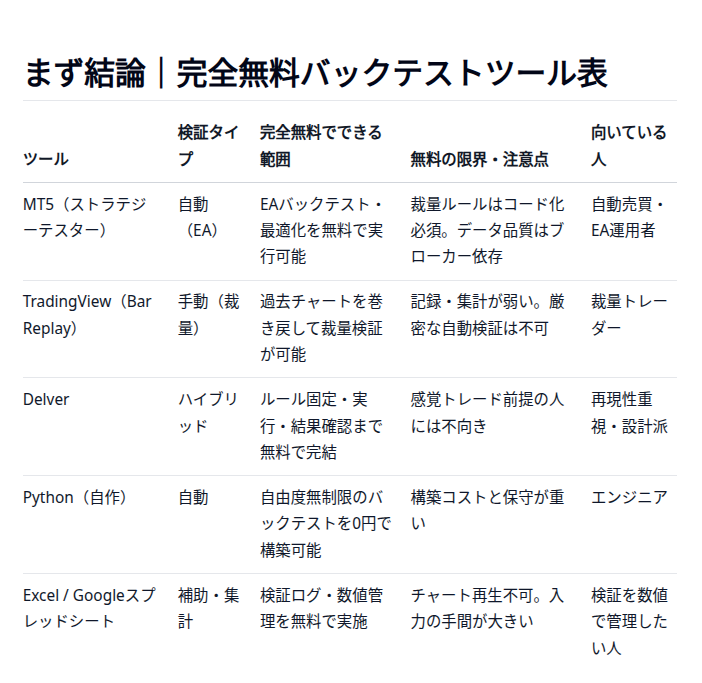

For recommended verification tools, please see the article below:

Why So Many People "Backtest But Still Lose"

Confusing "Backtesting" with "Looking at Charts"

When people hear the word "backtesting," they often think it means looking at historical charts and saying, "Ah, I would have won if I entered here."

This is not backtesting; this is just reflection. There is zero reproducibility in this approach.

Intuitive Verification Destroys Reproducibility

"This pattern looks strong."

"The vibe feels like it's going to trend."

The moment even one of these subjective judgments enters your process, your results become impossible to replicate under the same conditions next time.

The Cause is the "Design," Not the "Strategy"

Most people conclude that "this strategy didn't work." However, in reality:

- Conditions were vague.

- Exits were inconsistent.

- Records were non-existent.

Because of these factors, the data wasn't in an evaluable format to begin with.

Design Flaw #1: Vague Entry Conditions

Can You Describe the Entry in Writing?

First, ask yourself:

"Can I explain this entry condition to someone else in writing?"

- Which timeframe?

- At the exact moment which candle closes?

- What exactly needs to happen immediately before?

If you cannot verbalize this, the condition is unverifiable.

Lack of Fixed Parameters for Candles, Time, and Context

For example:

- What is the required wick length?

- What is the body-to-wick ratio?

- Is the setup treated the same in the Tokyo session as in London?

Without fixing these variables, you will produce a mass of trades that look similar but are fundamentally different.

Discretion Kills the Data

"The conditions are a bit weak this time, but let's try entering anyway."

The moment you allow this, your entire dataset becomes unreliable. In backtesting, the goal isn't to "trade well." The goal is to do the exact same thing mechanically, every single time.

Design Flaw #2: Changing Exits Every Time

Backtesting Without Fixed R-Multiples is Meaningless

Do you decide where to take profit based on the chart every time you enter? That is not backtesting; that is just discretionary trading on a past chart.

- How many pips (or what R) for the Stop Loss (SL)?

- What is the target R for Take Profit (TP)?

- Do you use partial exits?

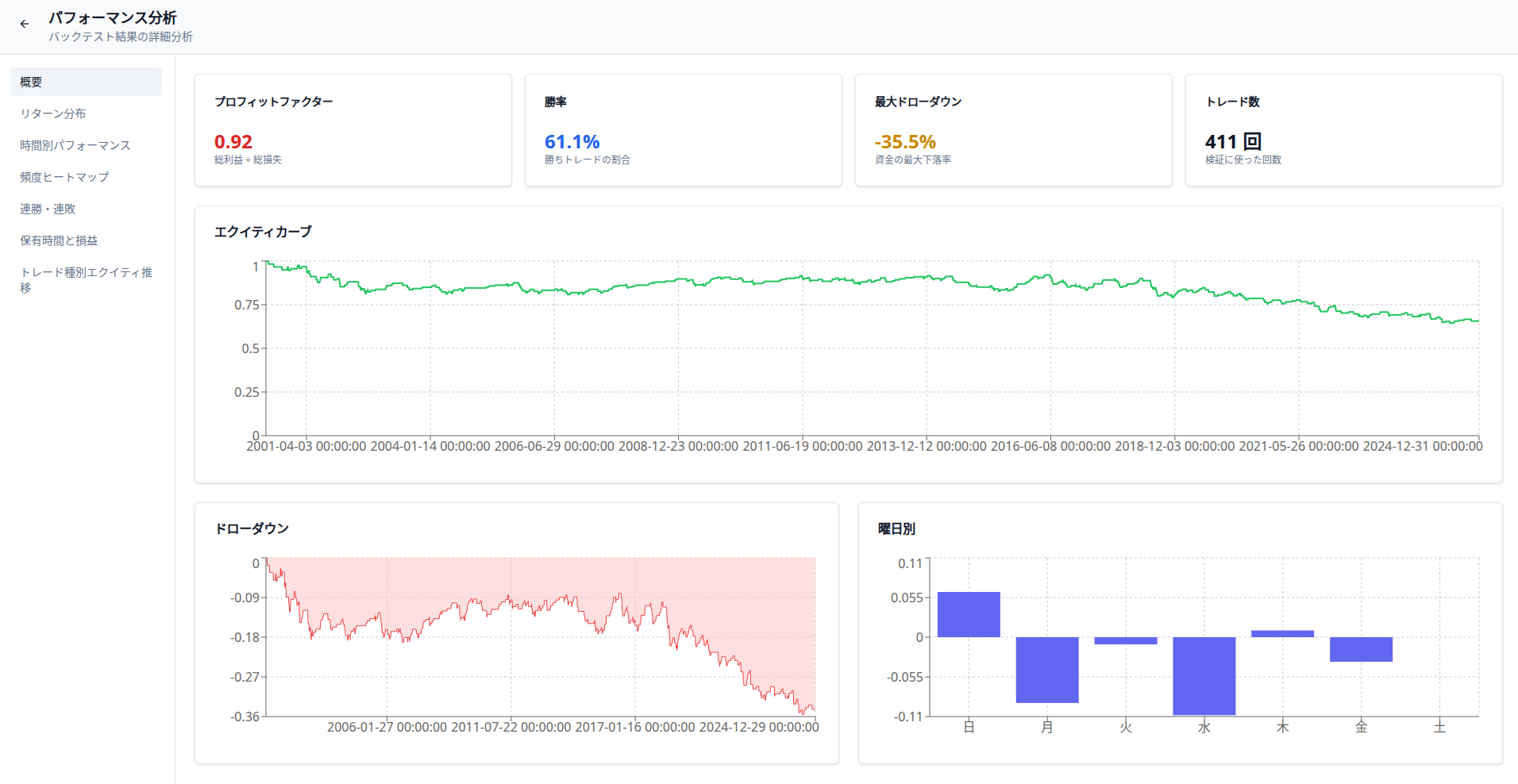

Without these rules, your win rate and Profit Factor (PF) become impossible to evaluate.

"Letting it Run Because it Looks Strong" is Not Backtesting

"It looked like it would trend, so I held for more profit."

Doing this creates a bias where:

- Winning trades are glorified.

- Losing trades are left as they are.

As a result, your results look better than they would actually be in real-time.

Ignoring "Time-Based Exits"

In real markets:

- Prices often go sideways for hours.

- Nothing happens after an entry.

If your design doesn't include time-based exits (e.g., exit after X candles), you will face unexpected losses and immense stress in live execution.

Design Flaw #3: Failure to Record and Aggregate Results

Looking Only at Win Rate, Ignoring PF and Drawdown

"A 60% win rate looks good." This is extremely dangerous.

- Profit Factor (PF)

- Maximum Drawdown (MDD)

- Maximum Consecutive Losses

Without these metrics, you cannot make any informed decisions regarding risk management.

Failure to Categorize Losing Trades

Do you categorize your losses into:

- Entry errors?

- Market environment mismatch?

- "Standard" losses within the system?

If not, the points that need improvement will remain invisible forever.

No Logs = Repeating the Same Mistakes Forever

Backtesting without records does not accumulate as experience. You will find yourself trapped in an endless loop of "I feel like I've lost in this exact spot before."

The Limits of Manual Backtesting and "The Next Step"

What Manual Backtesting Can and Cannot Tell You

Manual verification is good for:

- Getting a feel for the conditions.

- Filtering out obviously bad strategies.

However, it is fundamentally unsuitable for:

- Long-term performance tracking.

- Measuring Max Drawdown.

- Comparative fine-tuning of parameters.

Transition to Automated Backtesting

Once you reach the stage where:

- You can describe your conditions in writing.

- Your exit rules are fixed.

- You have finished over 100 manual tests.

There is no reason to stick to manual testing.

Conclusion

The reason you aren't winning despite backtesting is usually found in your Design, not your Trading Skill.

- Fix your conditions.

- Fix your exits.

- Keep detailed records.

Only when these three are aligned does backtesting truly become meaningful.